Industry News

Cignal AI: North American WDM transmission spending exceeds pre-pandemic levels

Views : 797

Author : JIUZHOU

Update time : 2022-08-26 15:22:03

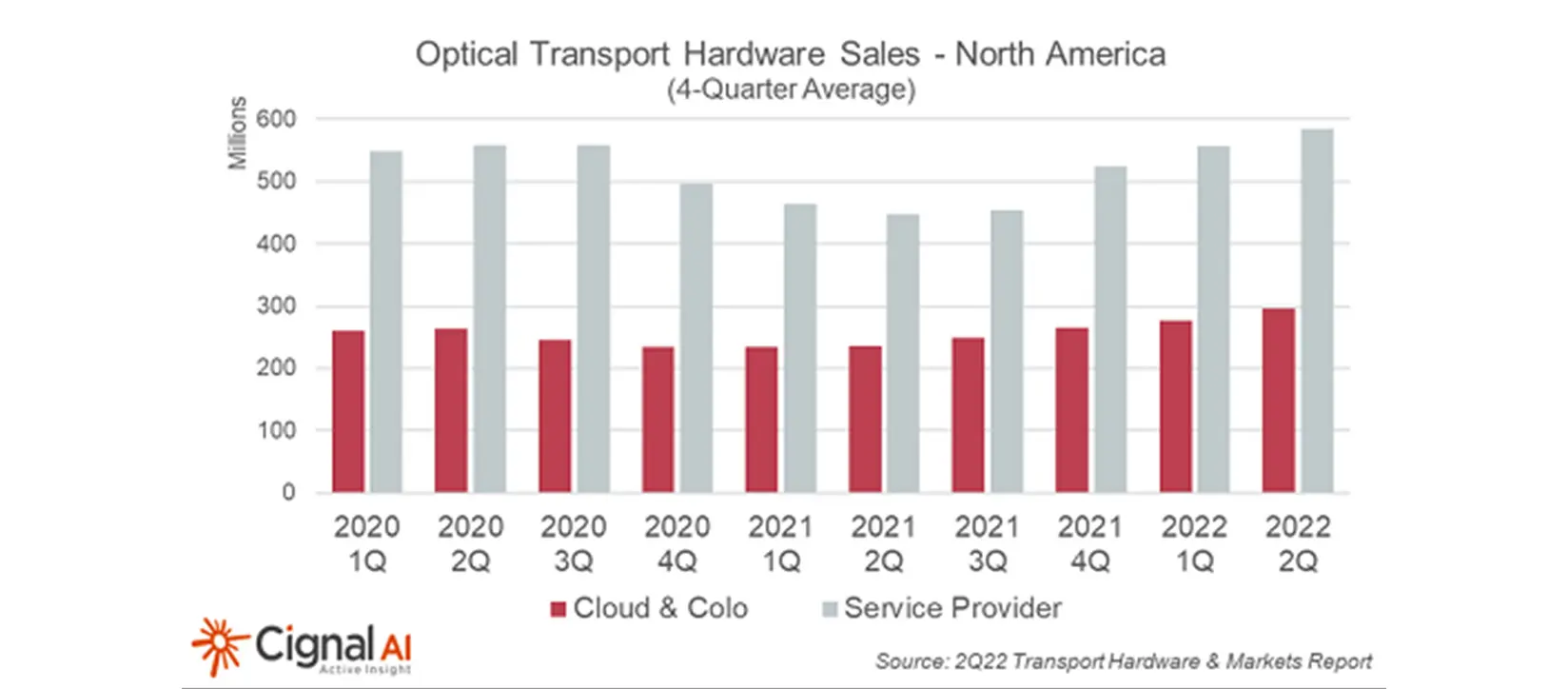

News takeaway: Equipment spending by legacy network operators and large cloud operators has now surpassed pre-COVID-19 levels in the second quarter of 2022. North American network operators spent more than 20% year-on-year on optical transport hardware, compared to weaker spending on optical and packet transport in EMEA and Asia.

Equipment spending by traditional network operators and large cloud operators has now surpassed pre-COVID-19 levels in the second quarter of 2022, according to research firm Cignal AI's latest transport hardware report. North American network operators' spending on optical transport hardware increased by more than 20% year-over-year, while European and Asian operators remained low in comparison.

Kyle Hollasch, principal analyst for transmission hardware at Cignal AI, said: "Capital investment in broadband infrastructure, the continued rollout of 5G, and pent-up demand from supply chain disruptions have driven growth in North American transmission spending. Large order backlogs and supply issues are expected to ease, It heralds a period of rapid spending growth for service providers and cloud operators in the region."

Orders remained exceptionally strong, with large suppliers generally reporting orders exceeding revenue, leading to record backlogs. Equipment suppliers said supply chain difficulties affected their ability to ship products and delayed network deployment and acceptance, delaying the recognition of some revenue.

Additional highlights from the Q2 2022 Transmission Hardware Report:

1. Global spending on optical hardware to grow 3% in the second quarter of 2022. Revenues rose in North America and China, while all other regions experienced declines.

2. Global cloud and Colo spending increased by more than 10% compared to roughly flat spending by traditional service providers. Revenues from the corporate and government segments fell year-over-year for the fifth consecutive quarter as (unusually high) spending levels during the pandemic returned to normal.

3. Cisco, Infinera and ADVA benefited the most from the increase in North American operator spending.

4. Results vary by region. North American optics revenue was the highest on record for the second quarter, while European spending fell. The decline in EMEA (Europe, Middle East and Africa) spending was due to the shift from transmission to RAN, as well as an unfavorable dollar exchange rate.

5. Global packet transport revenue increased 6%, driven by 16% growth in cloud and Colo packet spending.

6. North American packet transmission revenue grew by more than 30%, benefiting from Cisco, Nokia and Juniper. The EMEA packet transport market declined.

Equipment spending by traditional network operators and large cloud operators has now surpassed pre-COVID-19 levels in the second quarter of 2022, according to research firm Cignal AI's latest transport hardware report. North American network operators' spending on optical transport hardware increased by more than 20% year-over-year, while European and Asian operators remained low in comparison.

Kyle Hollasch, principal analyst for transmission hardware at Cignal AI, said: "Capital investment in broadband infrastructure, the continued rollout of 5G, and pent-up demand from supply chain disruptions have driven growth in North American transmission spending. Large order backlogs and supply issues are expected to ease, It heralds a period of rapid spending growth for service providers and cloud operators in the region."

Orders remained exceptionally strong, with large suppliers generally reporting orders exceeding revenue, leading to record backlogs. Equipment suppliers said supply chain difficulties affected their ability to ship products and delayed network deployment and acceptance, delaying the recognition of some revenue.

Additional highlights from the Q2 2022 Transmission Hardware Report:

1. Global spending on optical hardware to grow 3% in the second quarter of 2022. Revenues rose in North America and China, while all other regions experienced declines.

2. Global cloud and Colo spending increased by more than 10% compared to roughly flat spending by traditional service providers. Revenues from the corporate and government segments fell year-over-year for the fifth consecutive quarter as (unusually high) spending levels during the pandemic returned to normal.

3. Cisco, Infinera and ADVA benefited the most from the increase in North American operator spending.

4. Results vary by region. North American optics revenue was the highest on record for the second quarter, while European spending fell. The decline in EMEA (Europe, Middle East and Africa) spending was due to the shift from transmission to RAN, as well as an unfavorable dollar exchange rate.

5. Global packet transport revenue increased 6%, driven by 16% growth in cloud and Colo packet spending.

6. North American packet transmission revenue grew by more than 30%, benefiting from Cisco, Nokia and Juniper. The EMEA packet transport market declined.

Related News

Read More >>

Optical Connectivity: The Engine of AI Scaling

Optical Connectivity: The Engine of AI Scaling

May .08.2026

With the rapid growth of generative AI and large language models, data centers are quickly becoming intelligent computing centers. The growing demand for computing power from AI models is not just about performance.

5G Core & MEC: AI-Driven Growth Through 2030

5G Core & MEC: AI-Driven Growth Through 2030

Apr .17.2026

Global communications infrastructure is currently witnessing a long-awaited "second wave of explosive growth."

6G Outlook: The Future of Next-Gen Wireless Communication

6G Outlook: The Future of Next-Gen Wireless Communication

Apr .03.2026

The transition from 5G to 6G is more than just faster internet speeds. 6G will bring new changes to network design, operation, and business models. Wireless communication will become smarter, more efficient, and more energy-efficient.

Ready or Not, Next-Gen Communication Is Here

Ready or Not, Next-Gen Communication Is Here

Mar .20.2026

Standardization efforts for the next generation of mobile communication technologies commenced in 2025. They project commercial deployment to take place around 2030.